Are you planning to rent a car soon? One big question might be on your mind: will your insurance cover the rental car?

Understanding what your insurance does and doesn’t cover can save you from unexpected costs and stress. You’ll discover the key details about rental car coverage, what to look out for, and how to protect yourself. Keep reading to make sure you’re fully prepared before you hit the road.

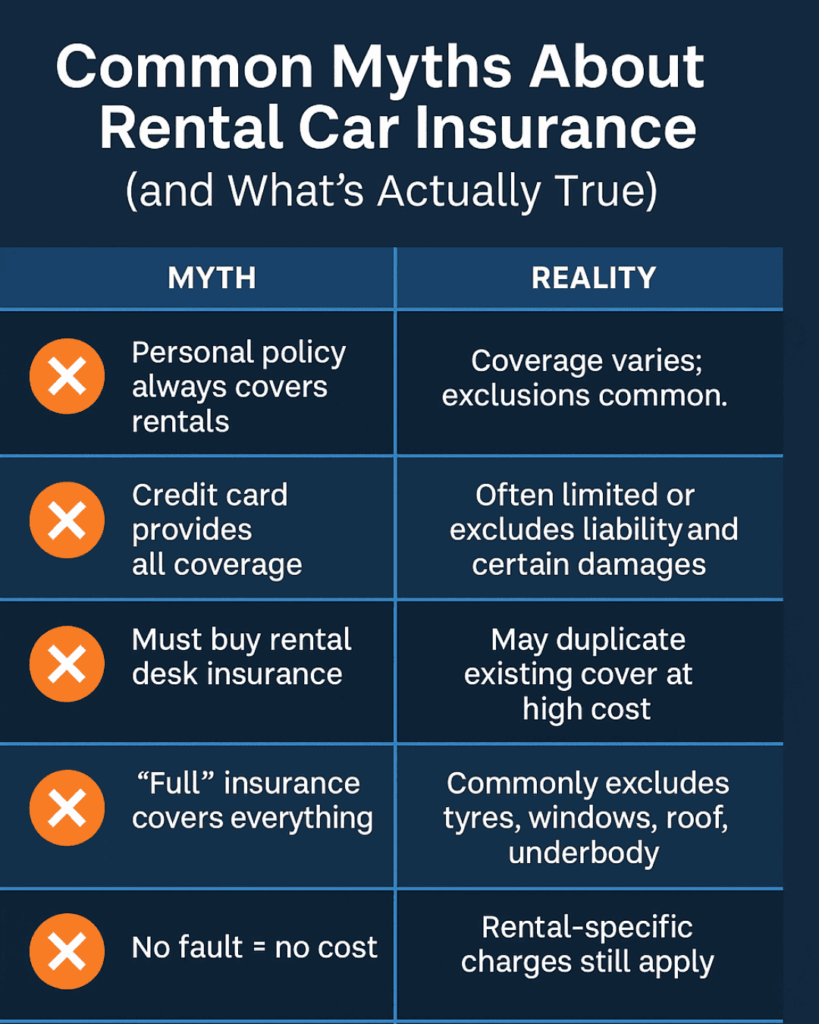

Types Of Insurance That Cover Rental Cars

Renting a car can be simple, but knowing if your insurance covers it is key. Different types of insurance might protect you during your rental period.

Understanding these insurance options helps you avoid extra costs and stay safe on the road.

Personal Auto Insurance

Your personal auto insurance often covers rental cars. It usually offers the same protection as your own vehicle.

This coverage can include liability, collision, and comprehensive insurance. Make sure to check your policy details before renting.

- Liability covers damage to others

- Collision pays for rental car damage

- Comprehensive covers theft and other losses

Credit Card Coverage

Many credit cards offer rental car insurance if you pay with the card. This can be a convenient way to get coverage.

Coverage depends on the card and may include damage and theft protection. Check your credit card terms to know the limits.

- Usually secondary coverage after personal insurance

- May cover damage and theft

- Some cards exclude certain vehicles or locations

Rental Company Insurance Options

Rental companies offer their own insurance plans. These can protect you if you lack other coverage.

Options often include collision damage waiver and liability coverage. Buying these can add extra cost but reduce risks.

- Collision Damage Waiver (CDW) covers car damage

- Liability coverage protects against third-party claims

- Personal Accident Insurance covers medical costs

Credit: www.trendrentals.com.au

When Personal Insurance Applies

Personal auto insurance can sometimes cover rental cars. This depends on the type of coverage you have. Knowing the details helps you avoid unexpected costs.

We will review when your personal insurance applies to a rental vehicle. Focus will be on liability, collision, and limitations.

Liability Coverage

Liability coverage usually transfers to a rental car. It protects you if you cause damage or injury to others. This coverage pays for their medical bills and repairs.

Most personal policies cover rental cars for liability. But this can vary by state and insurer. Check your policy for exact details.

Collision And Comprehensive Coverage

Collision and comprehensive coverage may apply to rental cars. This covers damage to the rental from crashes, theft, or weather.

- Collision covers damage from accidents.

- Comprehensive covers theft, fire, or natural disasters.

- Both require you to pay a deductible first.

- Some policies limit coverage to a certain rental period.

Limitations And Exclusions

Personal insurance may not cover every rental car situation. Some rules and limits apply. It is important to understand these before renting.

| Limitation | Description |

| Rental Period | Coverage may only last for a short rental time, like 30 days. |

| Vehicle Type | Luxury or large vehicles may not be covered. |

| Usage | Using the rental for business might void coverage. |

| Geographical Limits | Insurance may not apply outside certain areas or countries. |

Credit Card Rental Car Benefits

Many credit cards offer rental car insurance as a benefit. This coverage can save you money and stress during your trip.

It helps protect you from costs if the rental car is damaged or stolen. Knowing how it works is important before you rent.

How Coverage Works

Your credit card may cover collision damage and theft for rental cars. Coverage usually applies only if you pay for the rental with the card.

- The coverage is secondary in some cases, meaning it pays after your personal insurance.

- Some cards offer primary coverage, which pays first.

- Coverage limits and rules vary by card issuer.

- You must decline the rental company’s insurance to use your card’s coverage.

What Is Covered

| Type of Coverage | Details |

| Collision Damage | Repairs for damage caused by accidents |

| Theft Protection | Cost if the rental car is stolen |

| Loss of Use | Charges when the car is being repaired |

| Towing | Costs to tow the vehicle after damage |

| Exclusions | Damage to tires, windshield, or personal items may not be covered |

Steps To Use Credit Card Coverage

- Pay for the entire rental with your credit card.

- Decline the rental company’s collision damage waiver.

- Keep all rental documents and the police report if needed.

- Report any damage to your credit card company quickly.

- Follow up with the card issuer for claim instructions.

Credit: alphacarhire.com.au

Rental Company Insurance Explained

Renting a car often comes with extra insurance options. These protect you and the rental car in different ways. Knowing what each insurance covers helps you make better choices.

This guide explains three common types of rental car insurance. They are Loss Damage Waiver, Supplemental Liability Insurance, and Personal Accident Insurance.

Loss Damage Waiver (ldw)

Loss Damage Waiver is not traditional insurance. It is a waiver that protects you from paying for damage to the rental car. If you buy LDW, the rental company waives your financial responsibility for damage or theft.

LDW usually covers:

- Collision damage

- Theft of the rental car

- Vandalism or weather damage

- Towing costs after an accident

Supplemental Liability Insurance

Supplemental Liability Insurance adds extra liability protection. It covers damage or injury to others caused by you while driving the rental car. This insurance helps protect your assets from lawsuits.

| Coverage Type | What It Covers |

| Basic Liability | Minimum required by law, may be low |

| Supplemental Liability | Higher limits for bodily injury and property damage |

| Rental Company Offer | Usually includes Supplemental Liability for extra cost |

Personal Accident Insurance

Personal Accident Insurance pays for medical costs if you or your passengers get hurt in a crash. It can cover hospital bills, ambulance fees, and sometimes death benefits.

Key points about Personal Accident Insurance:

- Covers driver and passengers

- Includes medical and funeral costs

- Optional coverage beyond your health insurance

- May have limits on payout amounts

Factors Affecting Coverage Eligibility

Knowing if your insurance covers a rental car depends on many factors. Each factor can change how your coverage works or if it applies at all.

This guide explains key factors that affect your insurance eligibility for rental cars. Understanding these helps you avoid surprises.

Rental Duration And Location

Insurance coverage often changes based on how long you rent the car and where you drive it. Some policies limit coverage to specific times or places.

- Short-term rentals may have full coverage, while long-term rentals might need extra insurance.

- Driving outside your home country can void your existing insurance.

- Some states or countries require special coverage or have different rules.

Vehicle Type Restrictions

Not all rental vehicles qualify for insurance coverage. Your policy may exclude certain types or classes of vehicles.

| Vehicle Type | Coverage Allowed |

| Standard cars | Usually covered |

| Luxury or sports cars | Often excluded or limited |

| Large trucks or vans | May require special coverage |

| Motorcycles | Usually not covered |

Driver Qualifications

Your insurance might only cover drivers who meet certain qualifications. Age, driving record, and license status matter.

Common driver requirements for rental car coverage include:

- Minimum age, often 25 years or older

- Valid driver’s license held for at least one year

- No recent serious traffic violations or accidents

- Not under influence of drugs or alcohol

Credit: binscars.com

Claims Process For Rental Car Damage

Understanding your insurance coverage for rental car damage is crucial. Knowing the claims process can help you navigate incidents smoothly.

This guide will help you with the key steps in reporting, documenting, and resolving any disputes related to rental car damages.

Reporting The Incident

After an incident, reporting it promptly to your insurance provider is essential. This step ensures that your claim is processed efficiently.

- Contact your insurance company immediately.

- Provide details of the incident and any other involved parties.

- Take photos of the damage as evidence.

Documentation Needed

Proper documentation is key to a successful claim. Gather all necessary documents to support your case.

| Document Type | Details Required |

| Rental Agreement | Terms of rental and insurance coverage |

| Police Report | Details of the incident if applicable |

| Repair Estimates | Cost estimates for damages |

Handling Disputes

Disputes may arise during the claims process. Being prepared can help you resolve these efficiently.

Tips To Avoid Unexpected Costs

Renting a car can be tricky when it comes to insurance. Not knowing what your policy covers might lead to surprise costs.

To avoid these, make sure you understand your insurance policy and know your options before you rent.

Reading The Fine Print

Always read the details of your insurance policy. This helps you understand what is covered and what isn’t.

- Check for coverage on rental cars

- Look for exclusions like off-road travel

- Note any deductibles you must pay

Choosing The Right Coverage

Picking the right coverage for your rental car is important. Some policies offer different levels of protection.

| Coverage Type | Details |

| Collision | Pays for damage to your rental car |

| Liability | Covers damage to others |

| Personal Effects | Protects belongings in the car |

Using Third-party Insurance

Third-party insurance can be a smart choice. It might offer better rates or more coverage.

Consider these sources for third-party insurance:

- Credit card benefits

- Standalone car rental insurance providers

Frequently Asked Questions

Does My Personal Car Insurance Cover Rental Cars?

Most personal car insurance policies cover rental cars. Coverage depends on your policy type and limits. Check with your insurer to confirm.

Will My Credit Card Cover Rental Car Insurance?

Many credit cards offer rental car insurance as a benefit. Coverage varies by card type and issuer. Review your card’s terms carefully.

What Rental Car Insurance Does My Employer Provide?

Some employers offer rental car insurance for business trips. Coverage depends on company policy. Verify with your HR or insurance department.

Should I Buy Rental Car Insurance From The Agency?

Buying rental insurance is optional if you have coverage elsewhere. It provides extra protection and peace of mind. Assess your existing coverage first.

Conclusion

Knowing what your insurance covers can save money and stress. Read your policy carefully before renting a car. Some plans cover rental cars; others may not. Consider extra coverage if your policy falls short. Renting without proper insurance can lead to big bills.

Always ask the rental company about their insurance options. Stay safe and informed during your trip. This way, you avoid surprises and enjoy your ride worry-free.