Are you or a loved one wondering if Medicare covers in-home care? Understanding what Medicare pays for can be confusing, especially when it comes to care at home.

You want to make sure you get the help you need without unexpected bills. This article will clear up the confusion and give you straightforward answers about Medicare and in-home care. Keep reading to learn how Medicare works for home care and what options might be available to you.

Credit: www.vitalishealthcare.com

Medicare Basics

Medicare is a federal health insurance program. It mainly helps people 65 or older and some younger people with disabilities.

Many people wonder if Medicare covers in home care services. It is important to understand what Medicare offers and its plans.

What Medicare Covers

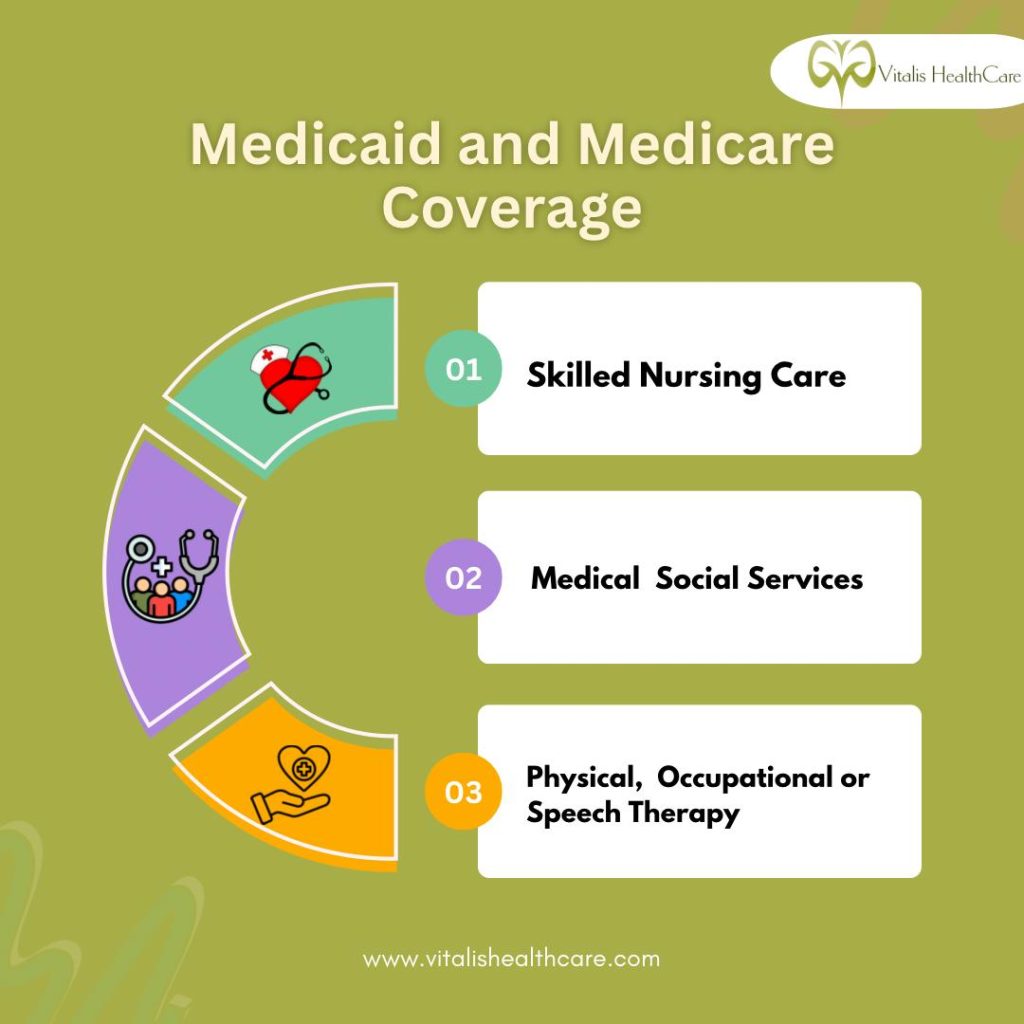

Medicare covers some types of home care, but not all. It usually covers care that is medically necessary and ordered by a doctor.

Covered services may include skilled nursing care, physical therapy, and some home health aide services. Medicare does not pay for personal care or homemaker services alone.

- Skilled nursing care at home

- Physical and occupational therapy

- Speech-language therapy

- Home health aide services with skilled care

- Medical social services

Types Of Medicare Plans

Medicare has different parts that cover different health needs. Knowing these parts helps you understand your coverage.

There are four main Medicare plans. Each plan covers specific services and costs.

- Part A:Hospital insurance that covers inpatient care, some home health care, and skilled nursing facilities.

- Part B:Medical insurance that covers doctor visits, outpatient care, and some home health services.

- Part C (Medicare Advantage):Private plans that include Parts A and B coverage, and often Part D. Some plans offer extra benefits.

- Part D:Prescription drug coverage.

Home Care Services Covered

Medicare helps pay for certain home care services. These services support people who need medical care at home.

Not all home care services are covered. Medicare focuses on skilled and medical needs, not daily chores.

Skilled Nursing Care

Medicare covers skilled nursing care at home if a doctor orders it. This care includes treatments by nurses.

Examples include wound care, injections, and monitoring health problems. Nurses help manage serious health issues.

Physical Therapy

Physical therapy helps improve movement and strength. Medicare pays for therapy at home if prescribed by a doctor.

Therapists create exercises and help patients recover from injury or surgery. Therapy aims to restore daily function.

Medical Social Services

Medical social services help with emotional and social problems related to illness. Medicare covers these services at home.

Social workers provide counseling, find community resources, and assist with care planning. They support patient well-being.

Eligibility For Home Care Benefits

Medicare offers some coverage for home care services. Not everyone qualifies. You must meet certain rules to get these benefits.

Knowing the requirements helps you understand if you can receive home care under Medicare.

Qualifying Conditions

To qualify for home care benefits, you need to have a medical condition that requires skilled care. This care must be given at home, not in a hospital.

- You must be homebound, meaning leaving home is hard and needs help.

- Your condition needs skilled nursing or therapy.

- You need a plan of care from a doctor.

- Care must be needed on a part-time or intermittent basis.

Doctor’s Certification

A doctor must certify that you need home care. The doctor writes a plan that states the care you require.

| Requirement | Details |

| Medical Need | Doctor confirms need for skilled care at home |

| Homebound Status | Doctor certifies patient is mostly confined to home |

| Plan of Care | Written by doctor and updated regularly |

| Recertification | Doctor reviews and renews need every 60 days |

Limitations And Exclusions

Medicare does not cover all types of in-home care. It has strict rules on what services it will pay for. Knowing these limits helps you plan better for care needs.

This section explains what Medicare excludes or limits under in-home care benefits. It covers non-skilled care, custodial care, and time restrictions.

Non-skilled Care

Medicare only pays for skilled nursing or therapy services at home. It does not cover non-skilled care like help with daily tasks. This includes assistance with bathing, dressing, or meal preparation.

Non-skilled care is often called personal care or homemaker services. These services are usually paid by Medicaid, private insurance, or out-of-pocket.

Custodial Care

Custodial care means help with activities like eating, toileting, or moving around. Medicare does not cover custodial care if it is the only care you need. It only pays if you also require skilled care.

- Custodial care alone is not covered by Medicare.

- Skilled nursing or therapy must be needed to get home care coverage.

- Custodial care can be covered by other programs or private pay.

Duration And Frequency Limits

Medicare limits how long and how often it covers home health services. Coverage depends on your medical needs and doctor’s orders. It does not pay for unlimited visits.

| Service Type | Limitations |

|---|---|

| Skilled Nursing Visits | Covered as needed with doctor’s approval |

| Physical Therapy | Limited to medically necessary sessions |

| Home Health Aide | Covered only with skilled nursing or therapy care |

| Duration | Coverage ends when care is no longer needed |

Costs And Out-of-pocket Expenses

Understanding what Medicare covers in home care is important. It helps you plan for costs and out-of-pocket expenses. These costs can vary based on the type of Medicare plan you have.

Medicare may cover some home care services, but there are still copayments and deductibles to consider. It’s essential to know these costs before planning your care.

Copayments And Deductibles

When using Medicare for home care, you might need to pay copayments. These are small fees you pay for each service. The amount can depend on the specific service you get.

Deductibles are amounts you must pay before Medicare starts covering costs. Once you pay your deductible, Medicare covers a part of your care expenses.

- Copayments are due at each service visit.

- Deductibles are paid yearly before coverage begins.

Medicare Advantage Plans

Medicare Advantage Plans might offer additional coverage for home care. These plans are provided by private companies. They must follow rules set by Medicare.

These plans often have different costs and benefits than standard Medicare. You should check what each plan offers to find one that suits your needs and budget.

- Medicare Advantage Plans may cover extra services.

- They often have varied premiums and benefits.

- Check each plan for specific home care coverage.

Credit: www.youtube.com

Alternatives To Medicare Home Care Coverage

Medicare may not cover all home care needs. Luckily, there are alternatives. These options can help support home care services.

Understanding these alternatives can ensure you get the care you need. Below are some common options to explore.

Medicaid

Medicaid offers home care services for those who qualify. It helps with both medical and personal care needs.

- Provides assistance with daily activities

- Covers medical equipment costs

- Offers long-term care support

Private Insurance

Private insurance may cover home care, depending on your plan. It’s important to review your policy details.

| Plan Type | Coverage Details |

| Comprehensive | Includes home nursing and therapy |

| Basic | May cover limited services |

Veterans Benefits

Veterans can access home care through specific benefits. These are designed to support those who have served in the military.

How To Apply For Medicare Home Care

Medicare can help pay for home care services. These services assist people who need help at home.

Knowing how to apply is important to get the care you need. Follow the steps below to apply.

Enrollment Process

First, you must be enrolled in Medicare Parts A and B. These parts cover hospital and medical services.

Next, you should contact Medicare or your local Social Security office to start the application. A doctor must certify that you need home care.

- Check if you have Medicare Part A and Part B

- Talk to your doctor about your home care needs

- Contact Medicare or Social Security to apply

- Complete the application with required information

Documentation Needed

You will need documents to prove your eligibility and care needs. These help Medicare decide if you qualify.

Important documents include medical records, proof of Medicare enrollment, and your doctor’s certification.

- Medicare card showing Part A and Part B enrollment

- Doctor’s statement explaining your need for home care

- Medical records supporting your condition

- Proof of identity, such as a government ID

Credit: www.youtube.com

Frequently Asked Questions

Does Medicare Cover All Types Of In-home Care?

Medicare primarily covers medically necessary in-home care, like skilled nursing or therapy. It usually doesn’t cover long-term personal care or homemaker services. Coverage depends on a doctor’s orders and specific health needs.

How Can I Qualify For Medicare In-home Care Coverage?

You must have a doctor’s certification that in-home care is medically necessary. You also need to be homebound and require skilled care services. Medicare requires a plan of care supervised by a healthcare professional.

What Types Of In-home Services Does Medicare Pay For?

Medicare covers skilled nursing care, physical therapy, speech therapy, and occupational therapy at home. It also covers medical social services and some home health aide services. Routine personal care and housekeeping are generally not covered.

Is There A Limit To Medicare’s In-home Care Benefits?

Yes, Medicare limits the number of covered visits based on your care needs. Coverage is typically short-term and tied to your condition’s improvement. Extended or long-term care needs usually require other insurance or payment methods.

Conclusion

Medicare covers some in-home care services but not all. It pays mainly for skilled nursing and therapy after hospital stays. Personal care and long-term help usually need other plans or payments. Understanding what Medicare covers helps avoid surprises later. Check your policy details carefully before choosing care.

Planning ahead keeps your care affordable and right for you.