Are you planning to rent a car soon? Before you hit the road, there’s one important question you need to answer: does your insurance cover rental cars?

Many people assume their regular car insurance or credit card will protect them, but the truth can be surprising. Knowing exactly what is covered can save you from unexpected costs and stress. Keep reading to find out how to avoid common mistakes and make sure you’re fully protected during your rental.

Your peace of mind on the road starts here.

Types Of Rental Car Coverage

Renting a car can be convenient, but it is important to know if your insurance covers it. Different types of coverage help protect you from costs if something goes wrong.

This guide explains the main types of rental car coverage. Knowing these can help you decide what protection you need.

Personal Auto Insurance

Your personal auto insurance may cover rental cars. It often extends the same protection you have on your own car to a rental vehicle.

This coverage usually includes liability, collision, and comprehensive protection. Check your policy details to confirm what is included.

- Liability covers damage to others and their property

- Collision covers damage to the rental car from accidents

- Comprehensive covers theft or damage not caused by a crash

Credit Card Benefits

Many credit cards offer rental car insurance as a benefit. This coverage often activates when you pay for the rental with the card.

Credit card rental insurance usually covers damage and theft. It may not include liability, so check the terms carefully.

- Damage and theft protection is common

- Liability coverage is usually not included

- Coverage may have limits on rental duration

- Check if you must decline the rental company’s insurance

Rental Company Insurance Options

Rental companies offer their own insurance plans. These can add extra protection but cost extra money.

Common options include collision damage waiver and liability coverage. These reduce your financial responsibility if an accident happens.

- Collision Damage Waiver (CDW) covers damage to the rental car

- Liability coverage protects you from claims by others

- Personal accident insurance covers medical costs

- Personal effects coverage protects your belongings inside the car

Credit: www.trendrentals.com.au

How Personal Insurance Applies

Many people wonder if their personal car insurance covers rental cars. The answer depends on the type of coverage they have. Understanding these details helps avoid surprises during a rental.

Your personal insurance often extends to rental vehicles. This includes liability and physical damage coverage. Still, limits and exclusions may apply.

Liability Coverage

Liability coverage protects you if you cause damage or injury while driving a rental car. Most personal policies include this coverage for rentals. It usually covers property damage and medical costs.

Check if your policy covers rental cars in other states or countries. Some policies limit coverage outside your home state.

Collision And Comprehensive Coverage

This coverage pays for damage to the rental car from crashes, theft, or other causes. Many personal policies include collision and comprehensive coverage for rentals. You might not need to buy extra protection from the rental company.

- Collision covers damage from accidents.

- Comprehensive covers theft, vandalism, and natural disasters.

- You must pay a deductible before coverage applies.

- Coverage may not apply to certain vehicle types like trucks or luxury cars.

Coverage Limits And Exclusions

| Coverage Type | Common Limits | Typical Exclusions |

| Liability | $100,000 per person / $300,000 per accident | Intentional damage, driving under influence |

| Collision | $50,000 per accident | Damage to tires, windshield, or rental truck |

| Comprehensive | $50,000 per incident | Personal items theft, roadside assistance |

Credit Card Rental Protections

Many credit cards offer rental car insurance as a benefit. This coverage can save money on extra rental insurance.

It is important to understand the rules and how this protection works before renting a car.

Eligibility Criteria

To use credit card rental protection, you must meet certain conditions. First, you must pay for the rental with the credit card.

The cardholder usually needs to be the primary renter on the contract. Some cards require the rental to be for a short period, like under 30 days.

- Pay rental with the credit card offering coverage

- Be the main driver on the rental agreement

- Rental duration often limited to 15-30 days

- Decline the rental company’s collision insurance

- Rental must be from an approved country

Coverage Details

Credit card rental protection usually covers damage and theft of the rental car. It may also cover towing and loss of use fees.

This coverage often acts as secondary insurance, paying what your personal car insurance does not cover.

- Collision damage to rental car

- Theft of rental vehicle

- Towing and loss of use fees

- Usually secondary to personal insurance

- Excludes personal injury and liability coverage

Claim Process

To file a claim, notify your credit card company soon after the rental incident. Provide all rental documents and damage reports.

The credit card company will review the claim and may ask for receipts, police reports, and photos.

- Contact credit card issuer quickly

- Submit rental agreement and payment proof

- Provide damage report and photos

- Include police report if theft or accident occurred

- Follow up for claim status updates

Credit: alphacarhire.com.au

Rental Company Insurance Plans

Many rental companies offer insurance plans to protect you while driving their cars. These plans cover different types of risks and damages. Understanding these options helps you choose the right coverage for your trip.

These insurance plans are separate from your personal car insurance or credit card coverage. It is important to know what each plan covers before you rent a car.

Collision Damage Waiver (cdw)

The Collision Damage Waiver lets you avoid paying for damage to the rental car. It covers costs if the car is damaged in an accident or by other causes like theft or vandalism.

- Usually covers repair costs

- May include loss-of-use fees

- Does not cover damage to other vehicles

- Often excludes damage from reckless driving

Liability Supplement

This plan protects you if you cause damage or injury to others. It covers legal fees and claims made by other drivers, passengers, or property owners.

| Coverage | Details |

| Bodily Injury | Covers medical costs for others hurt in an accident |

| Property Damage | Covers repairs to other vehicles or property |

| Legal Defense | Pays for lawyer fees if sued |

Personal Accident Insurance

This insurance covers medical costs for you and your passengers. It applies if someone is hurt in an accident while riding in the rental car.

Personal Accident Insurance usually includes:

- Medical expenses

- Emergency ambulance services

- Accidental death benefits

Common Coverage Gaps

Car insurance may not always cover rental cars fully. Many policies have limits and exceptions. These gaps can cause problems during a rental.

It is important to understand what your insurance does not cover. This helps avoid unexpected costs and stress.

International Rentals

Most personal car insurance policies do not cover rentals outside your home country. Driving abroad can expose you to risks not included in your policy.

- Liability coverage may not apply internationally

- Collision damage waiver might be excluded

- Additional local insurance may be required

- Roadside assistance often does not work abroad

Luxury And Exotic Cars

Insurance often excludes luxury and exotic rental cars. These vehicles are costly and have special coverage needs.

| Coverage Type | Standard Rental Car | Luxury/Exotic Car |

| Liability | Usually included | May be limited or excluded |

| Collision Damage Waiver | Often included | Usually requires extra coverage |

| Theft Protection | Included in many plans | Often excluded or limited |

| Roadside Assistance | Commonly included | May not cover exotic cars |

Underage Drivers

Insurance usually excludes drivers under 25 years old. Rental companies also charge extra fees for young drivers.

Key facts about underage driver coverage gaps:

- Many policies deny coverage for drivers younger than 25.

- Rental companies add “young driver” fees.

- Damage costs may not be covered if driver is underage.

- Special insurance or waivers might be needed.

Tips To Avoid Unexpected Costs

Renting a car can be confusing when it comes to insurance. Knowing what your insurance covers helps avoid surprise expenses. Let’s look at some steps to take before you rent.

These tips will guide you to check your policies, inspect the car, and understand your deductibles. Each step ensures a smooth rental experience.

Review Your Policies Before Renting

Check if your personal car insurance covers rental cars. Call your insurance provider to confirm. Some credit cards also offer rental car insurance. Make sure to review their terms.

- Contact your insurance company

- Read your credit card’s insurance policy

- Know the coverage limits

Inspect The Vehicle Thoroughly

Before driving off, check the rental car for damage. Look for scratches, dents, or other issues. Report any findings to the rental company to avoid charges later.

| Inspection Area | What to Check |

| Exterior | Dents and scratches |

| Interior | Seats and dashboard condition |

| Tires | Tread depth and pressure |

| Lights | Functionality |

Understand Your Deductibles

Your deductible is the amount you pay if there’s a claim. Knowing this helps you decide if extra insurance is needed. Compare the deductible to potential repair costs.

Credit: www.knellerins.com

Frequently Asked Questions

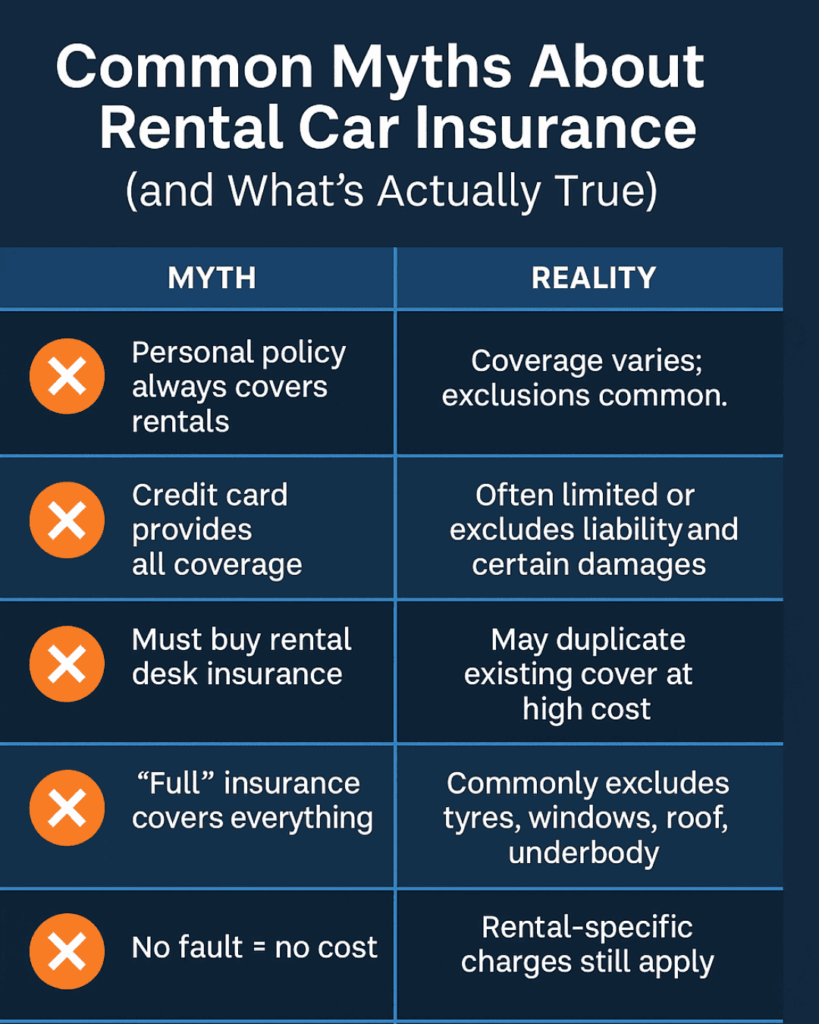

Does My Auto Insurance Cover Rental Cars?

Most personal auto insurance policies cover rental cars similarly to your own vehicle. Coverage usually includes liability, collision, and comprehensive. Verify your policy details before renting, as some restrictions may apply depending on the rental purpose and location.

Do Credit Cards Provide Rental Car Insurance?

Many credit cards offer rental car insurance as a benefit when you pay with the card. This coverage often includes collision damage waiver (CDW). Check your credit card terms to confirm coverage limits, exclusions, and how to activate the protection.

What Rental Car Insurance Is Mandatory?

Mandatory rental car insurance depends on the rental location and local laws. Liability insurance is often required by law. Rental companies may include basic coverage or offer additional insurance options. Always confirm requirements before renting to avoid unexpected costs.

Can I Decline Rental Car Insurance If Covered?

If your personal auto insurance or credit card covers rentals, you can usually decline the rental company’s insurance. Always carry proof of your coverage to avoid paying twice. Review your coverage carefully to ensure it meets rental car requirements.

Conclusion

Knowing what your insurance covers saves money and stress. Check your policy details before renting a car. Some credit cards also offer rental coverage. Decide if you need extra protection at the rental desk. This helps avoid surprise costs after an accident.

Always ask questions to understand your coverage fully. Stay safe and enjoy your trip with confidence.